Industry research

Scope

Europe

Companies

220

Table of contents

Report collaborator:

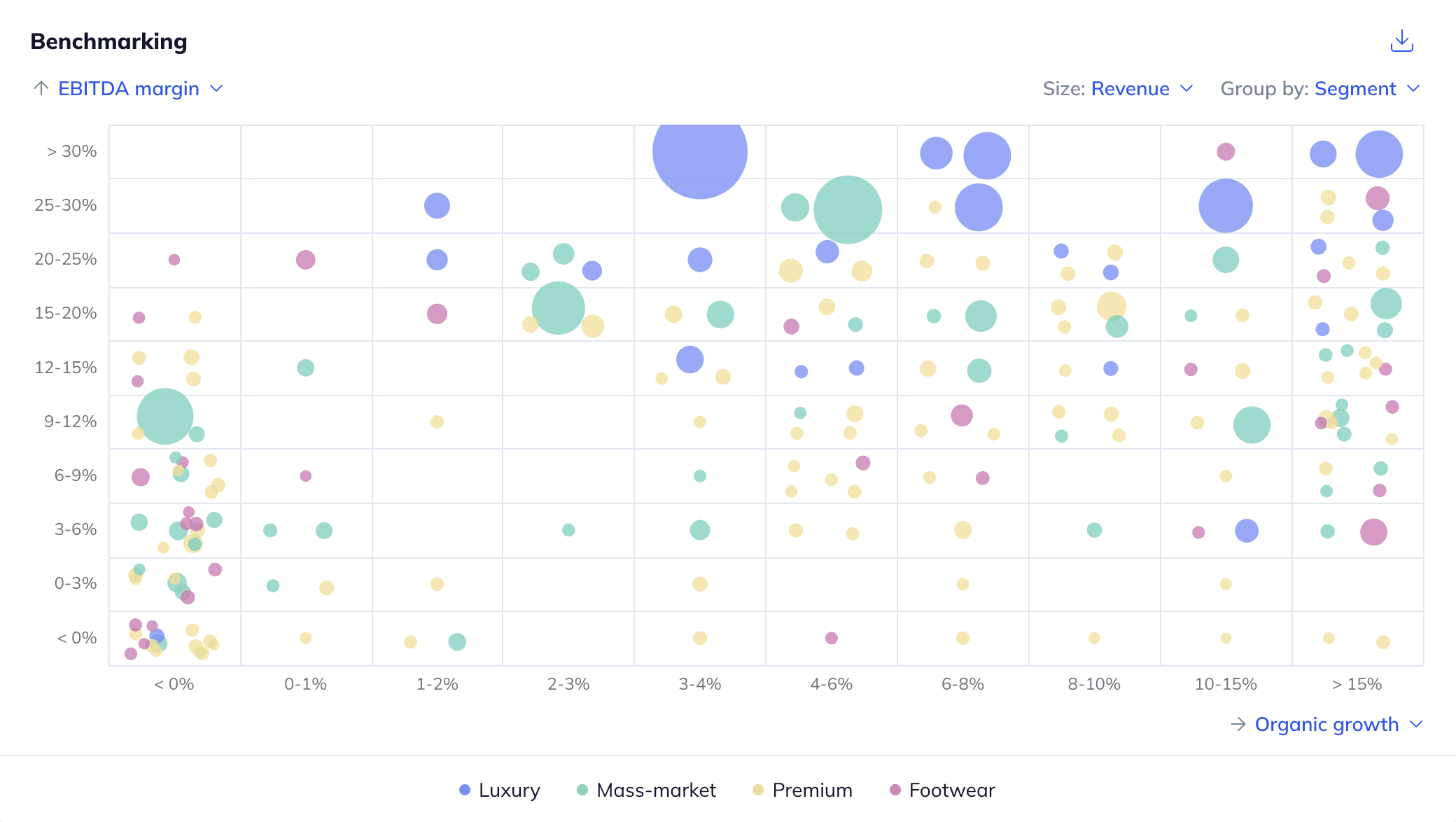

What does the fashion brands market landscape look like in Europe?

The European landscape has an overall fragmented nature, with the market for luxury fashion being an exception. Specifically, the luxury sector is dominated by multinational conglomerates (e.g. Kering, LVMH), despite the considerable presence of smaller independent brands. In other fashion segments, fragmentation arises from the wide variety of consumer needs that brands aim to satisfy. As competition intensifies, effective customer engagement is expected to become a critical factor for brands seeking to expand their market share. At the same time, the rise of second-hand marketplaces across all segments is likely to influence the sales volumes of traditional first-hand channels, reshaping the overall market dynamics.

What is the level of investor activity in Europe's fashion brands industry?

Sponsor-led interest has been moderate, with >40% of identified European assets being backed by financial sponsors (December 2025). Main risks for investors include the industry’s seasonality and cyclicality paired with the transactional nature of sales, as well as stringent EU regulation on fashion apparel, emerging resale competition and risks of counterfeits. On the other hand, bottom-line margin improvements on the back of D2C sales, opportunities stemming from the usage of data analytics to predict consumer behaviour and stable long-term underlying demand for clothing represent tailwinds for investors.

What are the key ESG considerations in Europe's fashion brands industry?

ESG topics mainly concern environmental and social matters. The fashion sector is one of the biggest emitters of greenhouse gases in the world with fast-fashion models acting as a main polluting force entailing overproduction, extended supply chains and low durability. In order to decrease their carbon footprint, brands need to lower product volume, extend their product lifecycles, improve sourcing processes and introduce second-hand offerings. From a social perspective, working conditions and employee safety in subcontractors’ facilities as well as fair buying practices are at the top of executives’ minds.

The European apparel market is expected to generate ~€463.9bn in revenue in 2025 and is projected to grow to ~€503.4bn by 2029 (~2.1% CAGR; Statista, December 2024)

The European footwear market is projected to grow from ~€126.7bn in 2025 to ~€162.8bn in 2030, registering a ~5.2% CAGR during the period (Statista, October 2025)

Demand for omnichannel shopping (e.g. mobile apps and in-store pick-up) is rapidly increasing, with ~90% of Europeans preferring a cross-channel approach. Omnichannel consumers make larger purchases compared to single-channel shoppers, making such strategies a strong revenue driver for brands (OC&C expert interview; E-commerce Germany, February 2024)

Growth opportunities in emerging markets on the back of stable underlying demand for clothing and footwear. By 2030, emerging markets are expected to add >50m new upper-middle class consumers, the core audience for premium and luxury brands (Bain & Company, November 2024)

Customer loyalty strategies present a vast growth opportunity for established brands. Industry experts estimate that players can potentially “double their business” by focusing on increasing their share of a customer’s spend through loyalty and engagement schemes (OC&C expert interview)

Stringent EU regulation to tackle the ESG impact of the fashion industry, including mandatory design standards to ensure longer-lasting products and measures to safeguard human rights across the value chain. This pressure requires investments in supply chains, traceability, technology and reporting, squeezing bottom-line profitability (European Parliament, September 2025; ASUENE, August 2025)

Resale platforms are increasingly embedded in consumer journeys, creating challenges for brands across all price points. As emerging and aggressive competitors, these disruptive platforms dilute brand control, weaken pricing power and reduce top-line growth for identified players (OC&C expert interview; interviews by Gain.pro)

Growing prevalence of counterfeit goods in the EU with the total value of seized fake goods estimated at ~€3.8bn in 2024 (+90% vs. 2022) with clothing accounting for ~7.5% of the total. Counterfeiters have established local manufacturing networks to produce near-indistinguishable counterfeits at lower prices, undermining the authenticity and value perception of brands (Novagraaf, February 2024; Modaes, October 2025; Glitz, October 2025)

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 220 private companies, incl. financials, ownership details and more.

A view on all 720 deals in the industry

ESG assessments with highlighted ESG outperformers